Is a 7% entry tax a deterrent or simply the price of admission to one of the world’s most resilient real estate markets? For the discerning investor, the extra Stamp Duty surcharges and the complexities of the Renters’ Rights Act 2025 aren’t roadblocks; they’re variables in a larger, high-yield equation. You likely recognize that while the UK offers unparalleled prestige and stability, finding a comprehensive non-resident buyer guide to UK property is the first step in managing an increasingly opaque landscape from abroad.

This strategic framework for 2026 is designed to transform complex tax liabilities and sourcing hurdles into a streamlined path toward asset ownership. We’ve distilled our LSE-educated insights into a sophisticated roadmap that covers everything from the 2% non-resident surcharge to securing off-market opportunities that never reach public portals. You’ll gain a clear understanding of the full financial commitment required and the legal nuances of the 2026 market, ensuring your next acquisition is defined by precision rather than friction.

Key Takeaways

- Understand the 2026 tax landscape, including the 2% non-resident and 5% second-home Stamp Duty surcharges, to calculate your total liability with precision.

- Use this non-resident buyer guide to UK property to move beyond public listings and access exclusive off-market assets and pre-sale opportunities.

- Shift from passive searching to strategic sourcing to mitigate the hidden costs of poor asset selection and lack of market transparency.

- Follow a structured acquisition framework that manages the heavy lifting of legal due diligence and professional instruction for a seamless experience.

- Leverage the intellectual authority of LSE-educated advisors to navigate complex market cycles and ensure your portfolio remains resilient.

The UK Real Estate Landscape for Global Investors in 2026

Entering the UK market in 2026 requires a departure from the buy-and-forget mentality of previous decades. A non-resident buyer status is strictly defined by the number of days spent in the country, but its implications reach into every corner of the transaction. From the mandatory digital record-keeping for high-earning landlords to the specific surcharges on acquisition, the regulatory environment has matured. This non-resident buyer guide to UK property serves as a compass for those who prioritize capital preservation over speculative gains. Success in this environment isn’t about speed; it’s about the intellectual rigor applied before the first offer is made.

Why the UK Remains a Global Safe Haven

The UK’s enduring appeal isn’t accidental. It’s built on the English Land Law Framework, a system that offers a level of transparency and protection rarely found in emerging markets. While other regions face political volatility or shifting property rights, the UK provides a composed environment for international wealth. Holding assets in Sterling remains a sophisticated diversification strategy, offering a steady hedge against fluctuations in North American or European portfolios. It’s a market defined by quiet confidence and a long-term horizon that rewards patient, well-advised capital.

Emerging Investment Hubs: Beyond the London Bubble

While London remains a prestige anchor, 2026 has seen a definitive shift toward high-yield regional centers. Cities like Manchester and Birmingham, alongside the “Golden Triangle” of Oxford and Cambridge, are no longer secondary choices. These hubs are benefiting from matured infrastructure projects that have fundamentally altered property valuations and rental demand. Accessing these markets requires localized intelligence that goes beyond basic online listings or public data. Utilizing a professional UK property sourcing service allows investors to identify assets with genuine growth potential before they hit the open market, ensuring the acquisition aligns with a broader wealth strategy.

The 2026 landscape demands a more calculated approach than in years past. With the Renters’ Rights Act 2025 now in full effect as of May 1st, the relationship between landlord and tenant has been recalibrated, abolishing no-fault evictions. This shift means that the quality of the asset and the tenant profile are more critical than ever. Investors must now look past the surface of a property to understand its long-term viability within a tighter legal framework. It’s an era where professional stewardship isn’t just a luxury; it’s the foundation of a resilient international portfolio.

Navigating the Legal and Financial Framework

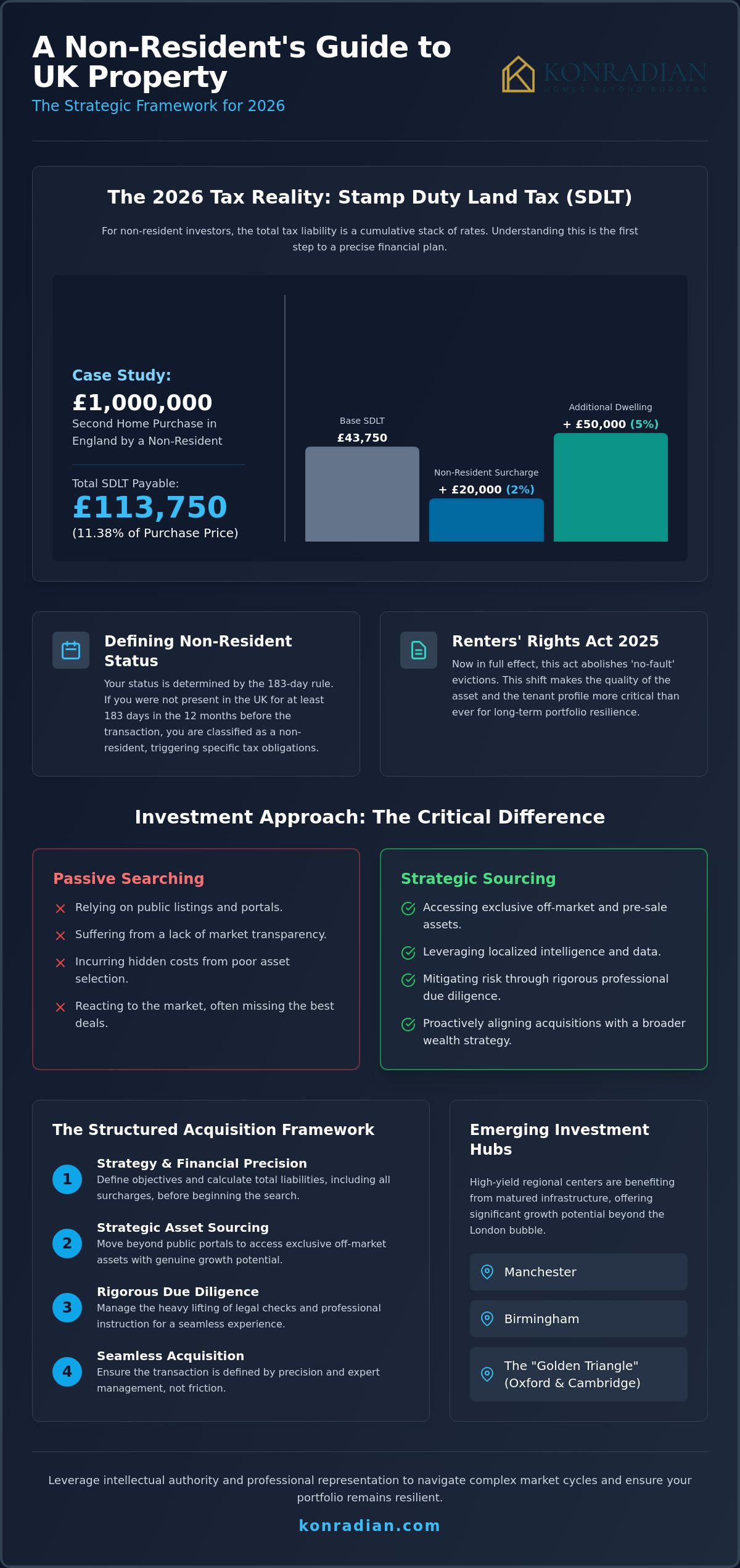

Understanding your specific tax and residency status is the cornerstone of a successful acquisition. In the UK, residency for property tax isn’t a matter of opinion; it’s a matter of mathematics. The 183-day rule serves as the primary benchmark. If you haven’t been present in the UK for at least 183 days during the 12 months prior to your transaction, you’re classified as a non-resident. This distinction triggers specific financial obligations that must be factored into your initial budget. This non-resident buyer guide to UK property focuses on ensuring these regulatory nuances don’t become expensive surprises during the closing stages of your investment.

The Reality of Stamp Duty for Non-Residents

Stamp Duty Land Tax (SDLT) is often the most significant entry cost for international investors. For most non-resident buyers, the tax liability is a cumulative “stack” of different rates. You’ll face the standard residential rates, a 2% non-resident surcharge, and, in many cases, a 5% surcharge for additional dwellings if you already own property elsewhere in the world. This can significantly alter the capital requirements for a high-value asset.

Consider a £1,000,000 acquisition of a second home in England. The base SDLT is calculated at £43,750. When you add the 2% non-resident surcharge (£20,000) and the 5% additional dwelling surcharge (£50,000), your total tax obligation reaches £113,750. This represents over 11% of the purchase price. While some reliefs exist for specific corporate structures or multiple dwellings, the 2026 landscape is rigorous. You can review the latest thresholds and surcharge details through the official Non-Resident Stamp Duty Land Tax guidance to ensure your figures are precise.

Financing the Purchase: Mortgages for Overseas Buyers

Securing financing as a non-resident is entirely possible, though it requires a more structured approach than a domestic loan. Most UK lenders will offer a Loan-to-Value (LTV) ratio between 60% and 75% for international clients. This means you should prepare for a minimum deposit of 25% to 40%. Beyond the deposit, the “Source of Wealth” and “Anti-Money Laundering” (AML) checks are comprehensive. Lenders will require a clear, documented trail of how your investment capital was accumulated.

High-street banks often lack the flexibility needed for complex international income streams. Specialist international lenders or private banks are usually more adept at handling non-resident applications, offering bespoke terms that reflect your global financial position. Securing the right legal support buying property abroad is essential here, as your solicitor will need to coordinate closely with your lender to satisfy these stringent AML requirements. If you’re unsure how your current holdings impact your UK borrowing capacity, a preliminary consultation with a specialist advisor can provide much-needed clarity before you begin your search.

Strategic Sourcing vs. Passive Searching

A common misconception among international investors is the belief that the entirety of the UK property market is visible through a simple web browser. While portals like Rightmove and Zoopla are helpful for domestic residential moves, they often function as a “graveyard” for high-yield or prestige investment assets. By the time a premium property is uploaded to a public portal, it has likely already been vetted and bypassed by professional sourcing networks. This non-resident buyer guide to UK property advocates for a fundamental shift from passive searching to strategic acquisition. It’s the difference between accepting what’s left and choosing what’s best.

In many global jurisdictions, brokerage services are funded by the seller, which naturally aligns the agent’s interests with achieving the highest possible price. The UK’s bespoke sourcing model is different. It’s a buyer-paid service where your advisor acts as a dedicated fiduciary. This structure ensures that your representative’s loyalty remains entirely with you, focusing on price suppression and asset quality rather than a quick sale. Think of the sourcing fee not as an additional cost, but as a strategic investment designed to mitigate the “hidden costs” of poor selection or overpayment.

The Limitations of Public Property Portals

Public portals are inherently reactive. In the high-velocity market of 2026, the most desirable units in regional hubs like Manchester or Birmingham are frequently secured via “pre-sale” agreements. Non-residents searching independently often find themselves trapped in aggressive bidding wars for leftover inventory. Without a local presence, you’re competing against professional domestic buyers who can view a property and submit a clean offer within hours. This disadvantage is magnified for international investors who don’t have the luxury of immediate physical inspections or established relationships with local estate agents.

The Sourcing Advantage: Accessing Exclusive Inventory

True strategic sourcing relies on deep-rooted developer relationships and a reputation for closing transactions efficiently. This provides access to “off-market” inventory—properties sold quietly to preserve privacy or units released early to preferred partners before they reach the public eye. Our selection process is governed by an intellectual rigor that filters for yield, capital growth, and long-term liquidity. This methodical approach mirrors the sophisticated strategies used in other mature markets, such as US real estate investment from Europe, where professional representation is the standard for high-net-worth individuals. By the time we present an opportunity, the heavy lifting of market analysis and initial due diligence is already complete, allowing you to move with quiet confidence.

The Step-by-Step Acquisition Journey

The path to owning UK real estate as an international investor is a methodical progression that requires both patience and precision. Unlike many other global markets, the English system is characterized by a “Subject to Contract” period. This means neither party is legally bound until the formal exchange of contracts occurs. This non-resident buyer guide to UK property breaks down the acquisition into four distinct phases designed to provide security and transparency from start to finish.

- Phase 1: Bespoke Sourcing & Strategic Consultation. We begin by aligning your investment objectives with current market inventory, focusing on assets that offer genuine capital growth or yield.

- Phase 2: Due Diligence & Legal Instruction. Once a target is identified, we instruct specialized solicitors to begin title searches and local authority inquiries.

- Phase 3: The Offer & Negotiation. We manage the bidding process to secure the best possible terms, ensuring the “Subject to Contract” status is clearly understood.

- Phase 4: Exchange of Contracts & Completion. This final stage involves the transfer of funds and the legal handover of keys, marking the official transition of ownership.

Remote Due Diligence: Buying Without Traveling

In 2026, physical presence is no longer a prerequisite for a successful purchase. We utilize high-definition video consultations and immersive virtual walk-throughs to provide a comprehensive view of every asset. To ensure your peace of mind, we coordinate independent surveyors who provide detailed reports on the structural integrity and condition of the property. Managing the exchange of contracts across different time zones requires a steady, reassuring pace. We facilitate the digital execution of documents and ensure your funds are positioned correctly for a seamless completion, regardless of your location.

Navigating the “Gazumping” Risk

One of the inherent complexities of the English legal system is “gazumping.” This occurs when a seller accepts a higher offer from another buyer after already accepting yours, but before the exchange of contracts. It’s a frustrating scenario that can derail an investment. The most effective strategy to mitigate this risk is speed. By having a proactive solicitor and a clear “Source of Wealth” trail ready, we can move from offer to exchange as quickly as possible, effectively locking out competing bidders. Professional stewardship ensures that every administrative hurdle is cleared before it can cause a delay. If you’re ready to secure a prestige asset with a partner who handles the heavy lifting, explore our UK property sourcing and legal support services to begin your journey.

Elevating Your Portfolio with Professional Representation

Managing a high-stakes acquisition from a distance requires more than just a digital connection; it demands a partner who understands the intricate machinery of the UK market. The “heavy lifting” of a 2026 purchase involves reconciling cumulative tax surcharges, vetting off-market inventory, and managing the aggressive timelines of the English legal system. By the time you reach the final stages of this non-resident buyer guide to UK property, it’s clear that the most successful investors are those who prioritize professional stewardship over a solo approach. Expertise doesn’t just simplify the process; it protects the integrity of your capital.

The UK sourcing fee shouldn’t be viewed as a traditional transaction cost. Instead, it’s a protective measure against the expensive errors that often plague unrepresented international buyers. Whether it’s overpaying for a “graveyard” listing on a public portal or failing to account for the 5% second-home surcharge, the financial risks of an unguided purchase are substantial. Professional representation ensures that every decision is backed by data and intellectual rigor, shifting the focus from mere acquisition to strategic wealth preservation.

The Konradian Difference: Elite Global Expertise

We bring a cosmopolitan mindset to the local UK market, bridging the gap between sophisticated global investors and the country’s leading developers. Our team’s education at the London School of Economics (LSE) provides a unique analytical lens, allowing us to interpret market cycles and asset valuations with a level of precision that goes beyond standard brokerage. We don’t just find properties; we curate opportunities that align with a broader international portfolio. Our LSE-backed strategy for 2026 acquisitions focuses on identifying undervalued assets in high-growth regional hubs while rigorously auditing the full tax liability of every transaction. This end-to-end concierge experience ensures you remain informed and in control, without the burden of daily administrative management.

Next Steps: Your Private Consultation

Every successful investment begins with a clear, strategic alignment of goals. We invite you to a private, complimentary video consultation to discuss your specific objectives for the UK market. During this call, we’ll explore how our bespoke sourcing agreement can be tailored to your requirements, from identifying prestige residences to securing high-yield commercial assets. Our process is steady and methodical, designed to provide peace of mind through every phase of the acquisition. It’s time to move beyond the limitations of public searching and access the full potential of the 2026 market. Schedule your strategic UK property consultation today to begin your partnership with a trusted global advisor.

Securing Your Future in the UK Market

The 2026 UK property market offers a unique intersection of stability and growth for those who approach it with intellectual rigor. Successfully navigating this landscape requires more than just capital; it demands a deep understanding of the 7% cumulative Stamp Duty surcharges and the foresight to secure assets before they reach the public domain. This non-resident buyer guide to UK property has outlined a framework where precision and professional representation are the ultimate safeguards against market friction.

Our LSE-educated advisory team brings over five years of international transaction success to every acquisition, providing you with exclusive off-market developer access that remains hidden from the average buyer. We handle the heavy lifting of legal due diligence and strategic sourcing, ensuring your transition into the UK market is defined by ease and security. When you’re ready to elevate your portfolio, Secure your UK investment with Konradian’s bespoke sourcing service. Your path to a prestige UK asset is a deliberate journey, and we’re here to guide every step with quiet confidence.

Frequently Asked Questions

Can a non-resident buy property in the UK after Brexit?

Yes, foreign nationals can legally purchase property in the UK regardless of their residency status or visa situation. Brexit hasn’t altered the fundamental right for non-residents to own real estate. This non-resident buyer guide to UK property emphasizes that while ownership is open, the tax and regulatory frameworks are where the complexity truly lies for international investors.

How much Stamp Duty (SDLT) do non-residents pay in 2026?

In 2026, non-residents pay a 2% surcharge on top of standard Stamp Duty Land Tax (SDLT) rates. If the property is an additional dwelling, such as a buy-to-let or second home, an additional 5% surcharge applies. This means an international investor faces a total surcharge of 7% before standard residential rates are even applied.

Can I get a UK mortgage if I live abroad?

You can certainly secure a UK mortgage while living abroad, though lenders typically require a larger deposit. Most international buyers should expect a Loan-to-Value (LTV) ratio between 60% and 75%, meaning a deposit of 25% to 40% is standard. Specialist lenders often provide more flexible terms for non-resident income streams than traditional high-street banks.

Do I need to visit the UK to complete a property purchase?

You don’t need to be physically present in the UK to complete your purchase. Modern acquisition frameworks utilize high-definition video walk-throughs and independent surveyors to handle due diligence remotely. Legal documents can be executed digitally or through international courier services, allowing for a seamless completion from any global time zone.

What is the difference between freehold and leasehold for foreign buyers?

Freehold means you own the building and the land it sits on indefinitely. Leasehold, which is common for UK apartments, means you own the right to occupy the property for a fixed term, often 125 or 999 years. Understanding this distinction is vital for long-term valuation and capital growth, as leasehold properties involve ground rent and service charges.

Is buying property in the UK a path to residency or a visa?

Property ownership does not provide a direct path to UK residency or a specific visa. While a significant investment can be part of a broader wealth profile, the UK doesn’t currently offer a “Golden Visa” based solely on real estate acquisition. You’ll still need to meet standard immigration requirements if you intend to live in the country long-term.

What are the ongoing taxes for non-resident landlords in the UK?

Non-resident landlords are subject to UK income tax on rental profits, usually deducted at a 20% basic rate by agents under the Non-Resident Landlord Scheme. You’re also liable for Capital Gains Tax at 18% or 24% upon disposal. As of April 2026, those with rental income over £50,000 must also comply with Making Tax Digital reporting.

How long does the average UK property purchase take for an international buyer?

An international transaction typically takes between 8 and 12 weeks from the moment your offer is accepted to the final key handover. This timeline accounts for the “Subject to Contract” period, legal searches, and the coordination of international funds. Using a non-resident buyer guide to UK property and a proactive sourcing partner can often compress these timelines by ensuring all documentation is ready in advance.